– Is the study of how the government or public sector pays for or finance expenditures through taxes and borrowing .

Public finance adapts and applies the fundamental microeconomic theory of markets to the public sectors and government sectors.

In particular,this area of study analyses the efficiency of taxes and the market failure of public goods.

Public finance is also a key to the study of government stabilization polices that address the inflation and unemployment problems of business cycle.

THE FOLLOWING ARE THE FUNCTIONS OF THE GOVERNMENT.

The government makes sure it maintains peace and harmony by providing security among their people.

The government does it through employing policemen, armed forces, magistrate etc.

Administrative function,

The government is responsible for the day to day running of activities in the economy, i.e. the government sets different departments and sectors to enable it administer their activities in its economy.

Social function.

The government provides social needs such as education, health, housing etc.

Development function.

The government provides funds for projects like roads construction, rural electrification, irrigation etc.

DIVISION OF PUBLIC FINANCE.

Public finance is divided into four areas including

Public revenue

Public expenditure

Government budget

Public borrowing / debt

GOVERNMENT REVENUE.

Refers to the amount of money which received by the government from different sources.

The following are source of government revenue;

i) Tax: is a compulsory payment levied by the government on individuals or companies to meet the expenditure which is required for public welfare.

ii) Fees: Are all payment made to the government on any direct services rendered/provided. E.g. payment of road licenses, stamp duty.

iii) Fines: Are penalties imposed by the government to the low breakers.

iv) State property:(Also known as public property)is a property that is owned by all, but is is accessed and use is controlled by the state.An example is a National Park or National Stadium.

v) Selling of public good: Like government shares,Through privatization of public companies like Tanesco in 2005,National Micro-finance Bank (NMB) in Tanzania hence the amount of money earned is revenue.

vi) Profit obtains from government properties like bus stations and public buses like UDA,uses of roads and airports etc.

vii) Special assessment: It is amount of money charged to people living in an area for specific purpose.

viii) Internal loan from central Bank for different uses like government projects.

ix) External loan from International financial Institution WORLD BANK, IMF and Development bank.

x) Grant and gifts inform of cash.

xi) Foreign Investment

xii) Gambling.

TAXATION.

is the imposition or infliction of taxes.The process

whereby charges are imposed on individuals/property by legislative

branch of the state or federal government to raise funds for public

purposes.

The following principles or cannons are important for good tax system when tax is imposed it must fulfill the following conditions.

CANONS OF TAXATION (PRINCIPLE)

According to Adam smith there are four important canons of

taxation which are( canons of equity, certainty, convenience and

economy)and other additions like canon of productivity, elasticity,

flexibility, simplicity and diversity as discussed below.

1. Canon of Equity.

he principle aims at providing economic and social justice

to the people. According to this principle, every person should pay to

the government depending upon his ability to pay.

The rich class people should pay higher taxes to the

government, because without the protection of the government authorities

(Police, Defence, etc.) they could not have earned and enjoyed their

income. Adam Smith argued that the taxes should be proportional to

income, i.e., citizens should pay the taxes in proportion to the revenue

which they respectively enjoy under the protection of the state.

2. Canon of Certainty

According to Adam Smith, the tax which an individual has to

pay should be certain, not arbitrary. The tax payer should know in

advance how much tax he has to pay, at what time he has to pay the tax,

and in what form the tax is to be paid to the government. In other

words, every tax should satisfy the canon of certainty. At the same time

a good tax system also ensures that the government is also certain

about the amount that will be collected by way of tax.

3. Canon of Convenience

The mode and timing of tax payment should be as far as

possible, convenient to the tax payers. For example, land revenue is

collected at time of harvest income tax is deducted at source.

Convenient tax system will encourage people to pay tax and will increase

tax revenue.

4. Canon of Economy

This principle states that there should be economy in tax

administration. The cost of tax collection should be lower than the

amount of tax collected. It may not serve any purpose, if the taxes

imposed are widespread but are difficult to administer. Therefore, it

would make no sense to impose certain taxes, if it is difficult to

administer.

Additional Canons of Taxation

Activities and functions of the government have increased

significantly since Adam Smith’s time. Government are expected to

maintain economic stability, full employment, reduce income inequality

& promote growth and development. Tax system should be such that it

meets the requirements of growing state activities.

Accordingly, modern economists gave following additional canons of taxation.

5. Canon of Productivity

It is also known as the canon of fiscal

adequacy. According to this principle, the tax system should be able to

yield enough revenue for the treasury and the government should have no

need to resort to deficit financing. This is a good principle to follow

in a developing economy.

6. Canon of Elasticity

According to this canon, every tax imposed by the

government should be elastic in nature. In other words, the income from

tax should be capable of increasing or decreasing according to the

requirement of the country. For example, if the government needs more

income at time of crisis, the tax should be capable of yielding more

income through increase in its rate.

7. Canon of Flexibility

It should be easily possible for the authorities to revise

the tax structure both with respect to its coverage and rates, to suit

the changing requirements of the economy. With changing time and

conditions the tax system needs to be changed without much difficulty.

The tax system must be flexible and not rigid.

8. Canon of Simplicity

The tax system should not be complicated. That makes it

difficult to understand and administer and results in problems of

interpretation and disputes. In India, the efforts of the government in

recent years have been to make the system simple.

9. Canon of Diversity

This principle states that the government should collect

taxes from different sources rather than concentrating on a single

source of tax. It is not advisable for the government to depend upon a

single source of tax, it may result in inequity to the certain section

of the society; uncertainty for the government to raise funds. If the

tax revenue comes from diversified source, then any reduction in tax

revenue on account of any one cause is bound to be small.

SYSTEMS OF TAXATION.

There are mainly three tax systems.

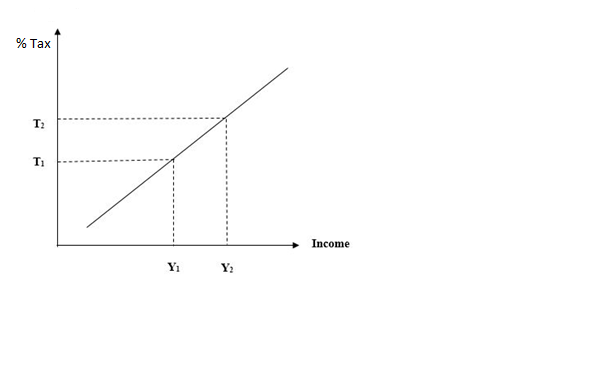

Progressive tax systems.

This is a tax system in which the tax rate increase with increase in income. It is aimed at reducing the gap between the rich and the poor (income gap) or income inequality.

Example of progressive tax is direct tax from income which is PAYE (Pay As You Earn).

It can be illustrated as follows.

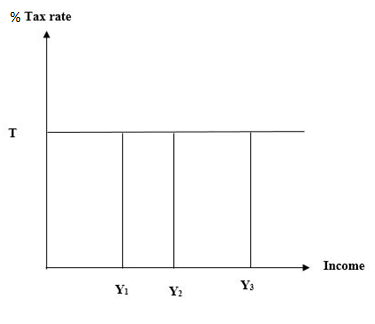

Proportional tax system.eg changes in income.

This is a tax system in which the tax rate is constant or fixed regardless of the changes in income. Aim to collect more money.

Proportional taxes maintain equal tax incidence regardless of the ability-to-pay and do not shift the incidence disproportionately to those with a higher or low economic well-being

Graphical illustration.

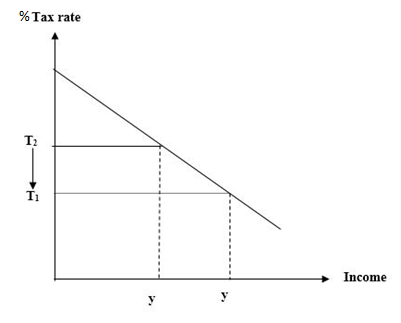

Regressive tax system.

A tax system where the tax rate decreases with increase in income (The higher the income,the low the proportional of the income is payed as tax and the low the income, the higher the proportional of the income is payed as tax.

It is mainly used to encourage investments.Example Social security tax ,for 2007 in USA,you pay 6.2% tax on wages up to a maximumu wage of$97,500.Therefore

(i) A person who makes $30,000 a year pays $1,860 (30,000 x 0.062) in tax or 6.2% of wages

(ii)A person who makes $200,000 a year pays $6,045 (97,500 x 0.062) in tax or 3% of wages.

(iii) A person who makes $500,000 a year pays $6,045 (97,500 x 0.062) in tax or 1.2% of wages.

Since the richest people pay the smallest percentage of their in tax,it is a regressive tax.

Requirement of a Good Tax Structure / System

The tax structure is a part of economic organization of a society and therefore fit in its overall economic environment.

No tax system that does not satisfy these basic condition can be termed a good one.

However, the state should pursue mainly following principles in structuring its tax system :-

1.The primary aim of the tax should be to raise revenue for public services.

2.People should be asked to pay taxes according to their

ability to pay and assessment of their taxable capacity should be made

primarily on the basis of income and property.

3.Tax should not be discriminatory in any aspect between individuals and also between various groups.

4.Tax system should be flexible and tax law should be clear and simple.

5.They should be comprehensive,it covers a wide tax base

6.They should be economical,should reduce the cost of tax administration

7.It should avoid double taxation.

TYPES OF TAX

1: DIRECT TAX.

Taxes which are imposed on incomes and personal property and whose burden is not shifted to another.

The direct tax includes

(a) Pay as you earn(PAYE)

(b) corporation tax

(c) Capital gain tax

(d) Agriculture revenue tax

(e) Death/estate duty.

(f) Property tax

(g) Inheritance duty

(h) Surtax. is the tax imposed on very rich person who earn much money.

ADVANTAGES OF DIRECT TAX.

It is economical i.e. cost of collection is minimum.

It is a source of revenue to the government

Tax payers know in advance the amount to be paid as tax

Most of direct taxes are progressive hence do not affect much the poor and hence reducing income gap.

Direct taxes are simple to understand

Helps to reduce demand pull inflation by reducing purchasing power of consumer.

Easy to determine the incidence of taxation.

DISADVANTAGES OF DIRECT TAX.

Discourage savings

Discourage people to work hard

Easy to evade

Discourage consumption as a result of decrease of disposable income

It discourages investment when charged on profit

It is not paid by all people i.e. unemployed are not paying

The burden of tax is highly felt

2. INDIRECT TAX.

Are taxes usually imposed on commodities. This tax can be passed from one person to another in terms of high prices.

This includes

Excise duty,- charged on local produced goods

Sales tax on locally produced goods on selling

Custom duty this includes import and export duty

Value added tax.

ADVANTAGES OF INDIRECT TAX.

Not easy to evade.

They results into higher level of revenue

It is convenient to pay by tax payers.

The effect of the tax is felt by consumers.

They are used to control the consumption of harmful products.

They are used to protect domestic industries.

They are used to stabilize the economy through increase and decrease of custom duty.

They encourage people to work hard i.e. the higher the price of commodities the harder people will work.

They are useful in control of allocation of resources.

DISADVANTAGES OF INDIRECT TAX.

Indirect tax are regressive or proportional ie the poor and rich pay the same amount hence affecting the poor.

It leads to cost push inflation.

They encourage black market, this occurs when indirect taxes are highly imposed.

Indirect taxes are not easily to determine who bares the incidence of the tax.

Discourages industrialization when tax imposed on goods produced hence high cost of production.

Indirect tax save time and lead to misallocation of resources since investors may invest in low tax areas.

It leads to inconvenience to businessmen because it requires a follow up.

Qn : Why do most LDCs depend on indirect tax more than direct tax. Disadvantages of direct and advantages of indirect tax.

VALUE ADDED TAX (VAT)

Is the tax imposed on the value added on commodities at different stages of production.

It is the tax valued at each stage of production.

VAT is only paid and accounted from registered VAT tax payers.

VAT is remitted by the tax payers within a period of one month from the day of purpose.

VAT is imposed on sales at every stage of production each cost is final consumer inform of high prices.

VAT is a tax on expenditure, it is a tax goods and services at each of production.

ADVANTAGES OF VAT.

It widens the tax base, it reaches many consumers.

It easy to calculate when records are available.

It is non discriminative to factors of production, since their taxed equally.

It encourages traders to keep books of accounts.

It shifts the incidence right away to the consumer ( it is easy to know the final payer of tax).

It enables tax payer to use government revenue before remitting the amount of tax offices.

It enables some goods to enjoy tax exemption.

It minimizes tax evasion since traders would pay for demand or receipts.

DISADVANTAGES OF VAT.

The tax is proportional hence affect the small firms.

It leads to increase in prices.

It is not economical.

It is not easy to understood by tax payers (consumers).

It delays government revenue since tax payers remit the amount after a given time.

It affects the level of consumption in the country due to high price.

IMPORTANT TERMS IN TAXATION.

TAX EVASION.

Is a situation where tax payer refuses to pay the tax assessed to her/him by tax officers. It is illegal.

TAX AVOIDANCE.

Is a situation where a tax payer falls to pay tax using the loophole in the tax law. It is not illegal.

. SPECIFIC TAX

This is a tax of a fixed amount per unit purchased.

AD VALOREM TAX

This refers to a tax which is based on the value of the goods it is percentage tax for example, sales tax, property tax etc.

THE BURDEN OF A TAX.

Refers to the feeling of tax payer as he/she pays the tax.

TAX BENEFIT PRINCIPLE.

It state that ‘the amount of tax paid by tax payer should be related directly to the benefit the tax pay will get after the government has spent its revenue.

ABILITY TO PAY PRINCIPLE

It state that, ‘the tax imposed on tax payers should be according to their taxable capacity i.e. high income earners higher taxes and lower income earns lower taxes.

INCIDENCE OF TAXATION.

Refers to the burden to pay tax, the final payer of the tax i.e. when a tax is paid who actually pays the tax.

The incidence of tax can either be formal incidence (among burden) or effective incidence (final resulting of the tax)

The incidence of tax can be seen in the following cases case of direct.

Case of direct tax.

In case of direct tax the incidence rest on the person who pays the tax first. It can be shifted to someone else.

Case of indirect tax.

In indirect tax the incidence can be shifted into two ways

There are

Forward shift: is a situation where the tax burden is shifted to final consumer inform of high prices.

Background shift: as tax is imposed the seller, negotiate with the producer to lower the price.

The incidence of a tax under indirect tax can be shifted either to the supplier or buyer (consumer). This shifting will depend on elasticity of demand for the commodities concerned, this can be good shown as follows:-

When the demand is elastic.

Elastic demand refers to the elasticity where a small change in price (increase or decrease) leads to big change in quantity (increase or decrease.)

When commodities have elastic demand the burden of tax is born by the seller and cannot be shifted to the buyer. An increase in tax means an increase in price leading to a big increase in quantity demanded.

Illustration;

When the demand is perfectly inelastic.

Perfectly inelastic demand refers to the elasticity in which price changes do not change the quantity demanded.

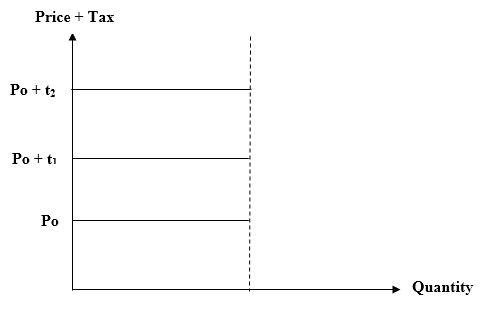

This is the demand of necessary goods which do not have substitute. In case of such goods an introduction of tax would lead t an increase in price and the burden of the tax is shifted to the buyer.

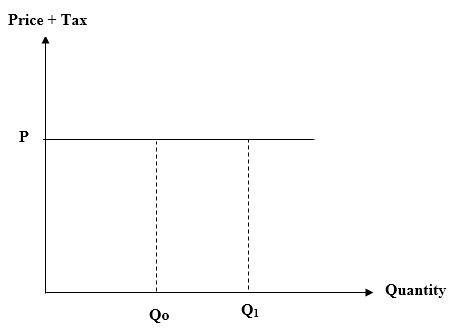

When the demand is perfectly elastic.

Perfectly elastic refers to elasticity in which the price remains constant with changes in quantity. The whole burden of the tax is paid by the supplier.

When the demand is inelastic

The elasticity of demand of commodity is said to be inelastic when a big change in price leads to a small change in quantity demand. In this case the burden of tax falls to the buyer (consumer)

THERE ARE FACTORS THAT MAY DETERMINE THE SHIFTING OF THE INCIDENCE.

The market power of the buyers and sellers.

For a case of monopoly the whole burden is shifted to the buyer through price discrimination while under perfect competition it taken by supplier.

The tax base

If the tax base is narrow its difficult to shift the tax burden i.e. if few commodities are taxed and a tax is introduced on other commodities the tax payer would substitute those tax commodities with untaxed commodities and vice versa.

WHY PAYING TAX. (Positive effect of tax)

To increase government revenue

To control harmful goods

To reduce the gap between the rich and the poor

To enable the government to provide public services

To control importation of goods and hence correct the balance of payments

To protect domestic and infant industries

To control allocation of resources

Stabilizing the economy.

NEGATIVE EFFECTS OF TAXATION.

It discourages savings

It discourages hard working

It discourages investment

It can lead to illegal activities

It may cause inflation

It may cause political and social stability in case the revenue is not spent property.

TAXABLE CAPACITY.

Refers to the ability of a nation to obtain revenue from tax payers necessary for its expenditure.

It is the ability of the tax payer to pay the taxes imported on him

Refers to the limits of a country capacity to accept and absorb taxation.

THE FOLLOWING ARE FACTORS AFFECTING TAXABLE CAPACITY.

The real wealth of a country i.e. resources

The size of population. The higher the population the higher taxable capacity this depends with the fraction of population engaged in economic activity

The level of economic development of the country

The possibility of tax evasion and corruption

The level of income when is low the lower the taxable capacity

The attitude of the tax payers in the payment of taxes

Income distribution in the country

Level of inflation.

Qn. Discuss why the taxable capacity is low in less developed country

Qn. Discuss the measure of the country can adopt to widen tax base and increase taxable capacity.

II. PUBLIC EXPENDITURE.

Refers to the spending by the government .it is categorized into two groups.

Recurrent expenditure.

Refers to government expenditure on public consumption like in education, salaries, health etc

Development expenditure

Is the expenditure by government on development projects like roads, in communication etc.

Roles of government expenditure (why should spend?)

To regulate economic activities

It influencing the allocation of resources

To enable government to maintain it enterprises and property

Provide essential goods and services to the public.

Stabilizing the economy

Motivating the government employee in terms of reward, seminar etc

To balance the national development.

III. NATIONAL BUDGET

It is the estimate of the government revenue and expenditure within a given year (financial year)

This is a statement showing anticipated receipts and anticipated payments.

TYPES OF NATIONAL BUDGET.

There two main types of government budget (Balanced and unbalanced budget which includes (Deficit surplus budget)).

Surplus budget

This refers to budget in which the anticipated revenue is great than anticipated expenditure. This surplus budget implies that

There is going to be a reduction in price level

There is reduction in money supply

There is reduction in economic activities

There is going to be grants and gifts to other countries

This kind of budget is not found in LDCs.

Qn, Why do countries plan for surplus budget, what are the objectives of surplus budget.

Their aimed at reducing money supply (circulation)

To enable government finance development projects in the future

To enable government give grants, loans to other countries

To correct balance of payments

To discourage consumption of some goods

To control inflation through reducing aggregate demand

To help the government to get money and repay debts.

Surplus budget may lead to the following problems;

Unemployment

Depression

Decrease in money supply leading decrease in investment and saving

Decrease in aggregate demand leading to decrease in production

Increase in tax rate to maximize revenue.

Deficit budget

Refers to the budget in which the anticipated revenue is less than anticipated expenditure. It occurs when government estimated expenditure is greater than estimated revenue. This is mainly occur in developing countries like Tanzania.

Balanced budget is when the anticipated budget is equal to anticipated expenditure.Government estimated revenue Government proposed expenditure.

Most of the classical economist advocated balanced budget,which was based on the policy of ‘line within means’.According to them,government revenue should not fall short of expenditure.

This implies that;

The government is going to borrow more money within a financial year

There is going to be an increase in money supply resulting from increase in expenditure

There will be increase in price level

There will be increase in aggregate demand and unemployment

The government may sale its assets.

Qn. Why having a deficit budget in LDC’S.

A deficit budget is aimed at increasing level of aggregate demand

Increase level of supply

Aim at controlling deflation

Reducing the tax burden

Encouraging borrowing

Shifting the economy from depression recovery

Increasing economic activities

Qn. What are the causes of budgetary deficit in Tanzania

Qn. Discuss the functions of the budget

PUBLIC DEBTS.

Is the total borrowing by the government. This includes internal and external borrowing.

CLASSIFICATION OF DEBTS

1. INTERNAL DEBTS.

Is the total money which the government borrows from individual and institutions within the country.

2. EXTERNAL DEBTS

Is the borrowing of a money outside the country e.g. from WB, IMF, ADB (African development bank)

3. REPRODUCTIVE DEBTS.

These are debts which the government uses for productive activities that will generate revenue to repay back the debts.

4. NON REPRODUCTIVE DEBTS (dead weight)

This are debts used to finance activities that do not give the return e.g. weapons.

5. SHORT TERM DEBTS.

This is debts paid within short time.

6. LONG TERM DEBTS

These are debts paid after a long period of time for example 10year – 50year.

7. A FUNDED DEBTS

These are debts in which a specific time of repaying debts is not fixed to get the loan.

8. UN-FUNDED DEBTS

These are debts in which date of redemption is stated while receiving the loan.

9. VOLUNTARY AND COMPOLSORY DEBT

REDEMPTION OF PUBLIC DEBTS

Redemption of public debt refers to the payment of public debts

WAYS USED IN REDEMPTION OF PUBLIC DEPT.

1. REPUDIATION.

Repudiation is form of debt redemption where the government refuse to pay debts.

2. BY CONVERSION.

Is the form of debts redemption where the government takes new loan with low interest and paying the previous loan with higher interest.

3. NEGOTIATIONS ON DEBTS.

This refers to cancellation of a debt

4. USE OF SURPLUS BUDGET

Where the expenditure is less than revenue and extra amount of money is left for paying debt.

5. CAPITAL LEVY.

Is where the government imposes taxation on asset like building and the revenue is used to pay the debts.

6. SINK FUND

Is the situation where the government invest a given amount of money in the bank to get compound interest and hence use the amount obtained to pay a debts.

7. PRIVATIZATION OF PUBLIC GOODS.

The money obtained from privatization is used for debts repayment.

8. USE OF GRANTS AND GIFTS RECEIVED

9. SELLING SECURITY TO THE GOVERNMENT

10. USE OF ACCUMULATED FOREIGN RESERVES.

CAUSES AND JUSTIFICATION OF PUBLIC DEBTS.

Qn. Why do LDC’s government depend on borrowings?

-To increase revenue since tax revenue is not enough to finance government activities in LDCS.

-To reduce the tax burden from tax payers

-To correct balance of payment deficit,

-To reduce printing of more money by the government to avoid inflation.

-In order to overcome natural calamities such as drought etc.

-To help the government attain economic growth through the finding of more economic activities hence economic growth

-Enable the government persuade its development plan

-To balance the budget and cover budgetary deficits.

-To enable the government repay loan conversion

-To control economic depression through increase in aggregate demand result from increase in unemployment opportunities.

Qn. Discuss the roles played by public borrowing in LDC.

-It leads to over dependency

-It reduces money available for consumption and investment.

-Debts worsen the country balance of payment position.

-If the dept is not used reproductively it becomes a burden to the government and its people.

-Most of the debts are always in the form of a tied aid i.e. debt with conditions (strings attached)

-When the debt is long-term its burden is shifted to another generation

-There is a burden of paying interest and other cost in debts administration.

Qn. Discuss the measure your country is using to reduce debt burden?

Qn. Discuss why external debts have been increasing instead decreasing in LDCS

FISCAL POLICY.

-This is the use of taxation, government expenditure and public borrowing to influence the economic activity of a given country.

How fiscal policy work (mechanism of fiscal policy)

It works in two ways i.e. expand economic and to contract economy.

EXPANSION FISCAL POLICY

This is a situation where there is increase of government

expenditure and decrease in tax. It is aimed at increasing aggregate

demand.

II. CONTRACTION FISCAL POLICY.

It aimed at reducing aggregate demand where there is increase in tax and decrease in expenditure.

Qn. Discuss how fiscal policy can be used to bring economic development hint (use roles of tools of fiscal policy)

No comments:

Post a Comment